DEMAND AND RECOVERY FORMS

Guide to Rule 142 of CGST Rules 2017

The Goods and Services Tax (GST) system in India, governed by the CGST Act, 2017, aims to maintain proper tax compliance and enforce payment mechanisms. Rule 142 of the CGST Rules, 2017 plays a crucial role in the tax recovery process by regulating the issuance of notices, orders, and recovery actions. The rule is closely linked with the use of various DRC Forms (Demand and Recovery Forms), each of which has a specific purpose and procedure.

This article will explore Rule 142, the associated DRC Forms such as FORM GST DRC-01, FORM GST DRC-01A, FORM GST DRC-02, and others, along with the relevant sections of the CGST Act (including Sections 73, 74, 74A, 76, 122, 123, 124, 125, 127, 129, and 130) that guide the demand and recovery process under GST.

Rule 142 of the CGST Rules, 2017 provides the procedural framework for issuing electronic notices and orders under the GST regime. It establishes the system for tax officers to notify taxpayers about their tax dues, penalties, or discrepancies, and enables taxpayers to make payments or respond to these notices. The rule also outlines the procedures for recovering outstanding taxes

Key Features of Rule 142:

The rule incorporates various sections of the CGST Act, 2017, including Sections 73, 74, 74A, and others, which specify the circumstances for issuing recovery notices and actions.

Electronic communication of notices and orders.

Standardized DRC forms for initiating and resolving disputes.

Provides taxpayers with the opportunity to pay dues, file submissions, and request rectifications.

Overview of DRC Forms Under Rule 142

The DRC forms are designed to facilitate the communication process between tax authorities and taxpayers. Below are the key DRC Forms:

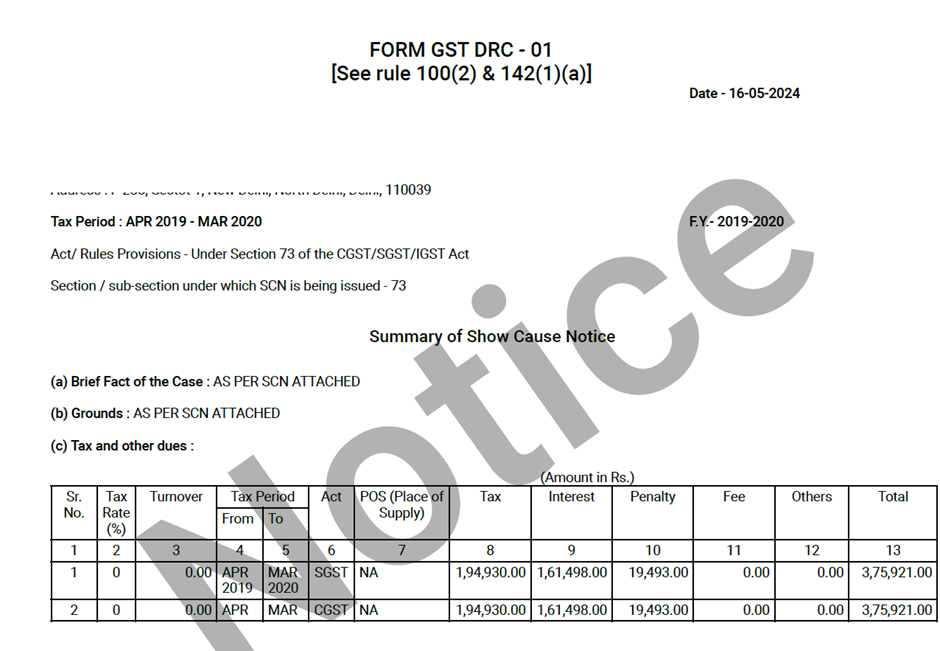

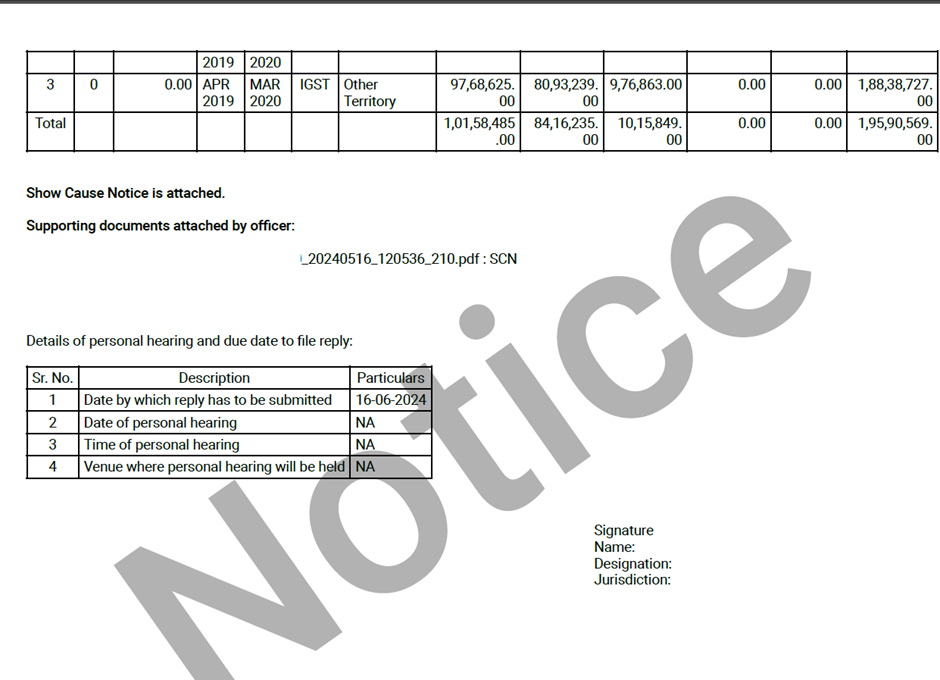

1. FORM GST DRC-01: Show Cause Notice for Demand of Tax

FORM GST DRC-01 is issued when there is a demand for tax payment due to discrepancies or non-compliance by the taxpayer. This form outlines the details of the tax demand and serves as a formal notice.

- Applicable Sections:

- Section 52: For defaults in TCS by e-commerce operators.

- Section 73: Determination of tax pertaining for not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised for any reason other than fraud or any willful-misstatement or suppression of facts

- Section 74: Determination of tax pertaining to the period up to Financial Year 2023-24 not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised by reason of fraud or any willful- misstatement or suppression of facts

- Section 74A: Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised for any reason pertaining to Financial Year 2024-25 onward

- Section 76: For tax collected but not deposited with the government.

- Sections 122-125: For penalties for procedural or reporting violations.

- Section 129: For detention and seizure of goods or conveyances in transit.

- Section 130: For confiscation of goods or conveyances in cases of tax evasion..

In the Show Cause Notice under FORM GST DRC-01, the officer must issue a summary of the notice in the form. This includes a clear explanation of the taxpayer’s liability, providing a detailed breakdown of the tax due, including the tax amount, interest, and any penalties. The officer shall provide the notice and include a summary of the notice in FORM GST DRC-01, specifying the exact nature of the discrepancies and the applicable sections of the law. The taxpayer is given a chance to respond, either by paying the dues or submitting necessary clarifications or documents.

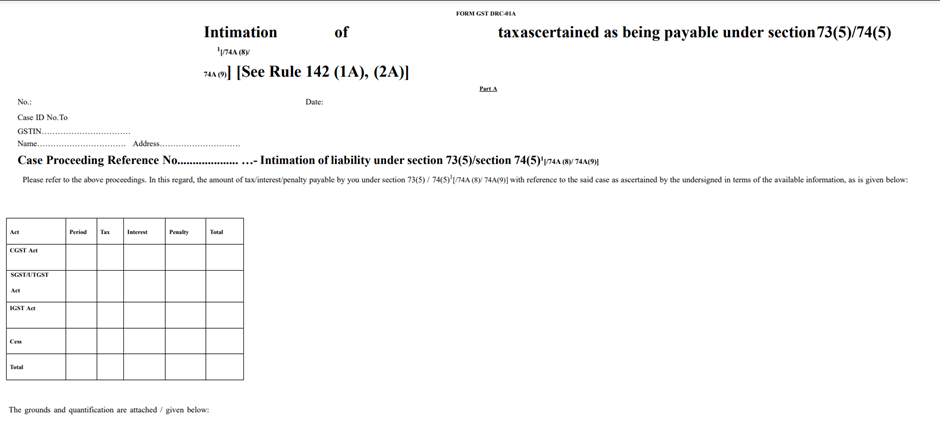

2. FORM GST DRC-01A: Pre-Notice Intimation

FORM GST DRC-01A is a pre-notice intimation issued by the tax officer before issuing FORM GST DRC-01. It serves as an early warning to the taxpayer, informing them of possible tax dues. The officer will outline the tax ascertainment (calculation of taxes, interest, and penalties) and provide the taxpayer with an opportunity to pay the dues voluntarily.

- Applicable Sections:

- Section 73: For cases involving non-fraudulent underpayment or incorrect claims.

- Section 74 & 74A: For cases where fraud or willful misstatement is suspected.

In FORM GST DRC-01A, the officer will state:

“You are hereby advised to pay the amount of tax as ascertained above along with the amount of applicable interest and penalty under Section 74(5) by [due date], failing which a Show Cause Notice will be issued under Section 74(1).”

If the taxpayer fails to comply with the provisions of FORM GST DRC-01A, the tax officer will initiate the recovery process by issuing FORM GST DRC-01.

3. FORM GST DRC-02: Summary of Show Cause Notice

FORM GST DRC-02 is issued when an officer issues a statement instead of a Show Cause Notice under Sections 73, 74, or 74A. This form provides a summary of the statement that includes a clear breakdown of the tax demand, interest, penalties, and other details that need to be paid. It serves to inform the taxpayer of their liabilities and provides them with the necessary details for compliance.

- Applicable Sections:

- Section 73: For non-fraudulent shortfall or errors in tax payment.

- Section 74: For fraudulent tax actions.

- Section 74A: For discrepancies for the financial year 2024-25 and onwards.

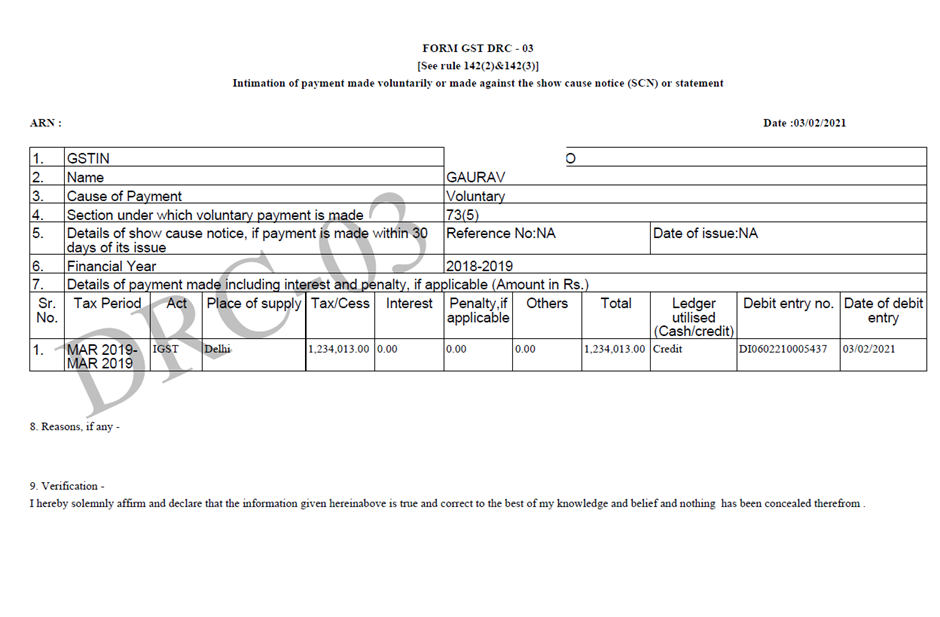

4. FORM GST DRC-03: Voluntary Payment Form

FORM GST DRC-03 is used by taxpayers to make voluntary payments of tax, interest, or penalties before or after the issuance of a show cause notice but before issuing DRC 07, because after issuance of Form GST DRC-07 filing of Form GST DRC-03A is mandatory.

- Applicable Sections:

- Section 73: Non-fraudulent underpayment.

- Section 74: Fraudulent underpayment.

5. FORM GST DRC-04: Acknowledgment of Voluntary Payment

Once a taxpayer makes a payment using FORM GST DRC-03, the authorities will issue FORM GST DRC-04 as an acknowledgment of the voluntary payment. This ensures that the taxpayer’s payment has been recorded.

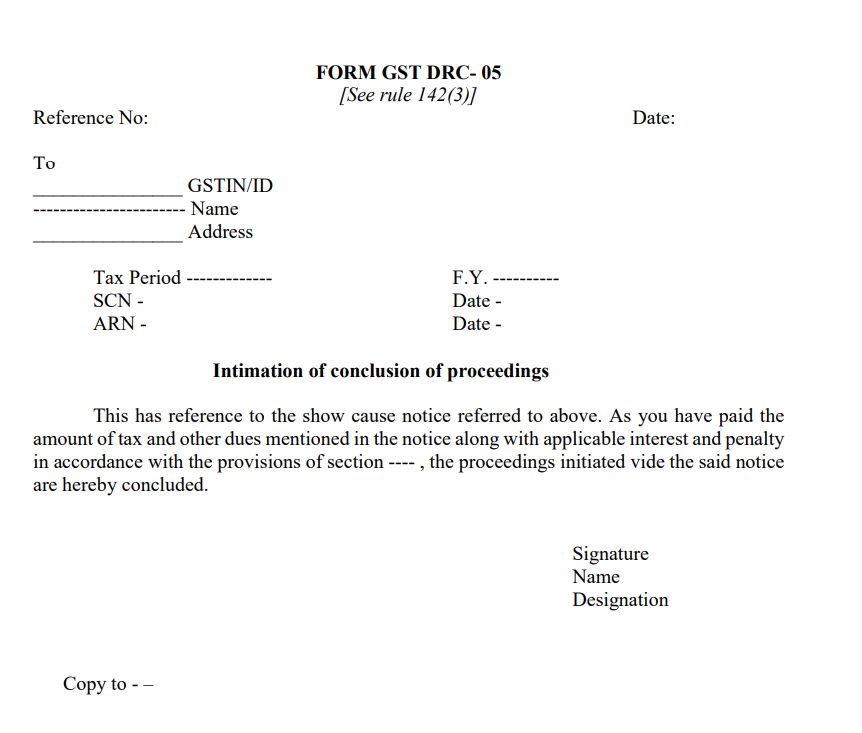

6. FORM GST DRC-05: Closure of Proceedings

After the payment of tax dues under FORM GST DRC-03, if there is no dispute, the proceedings will be closed, and FORM GST DRC-05 will be issued to the taxpayer to confirm the closure.

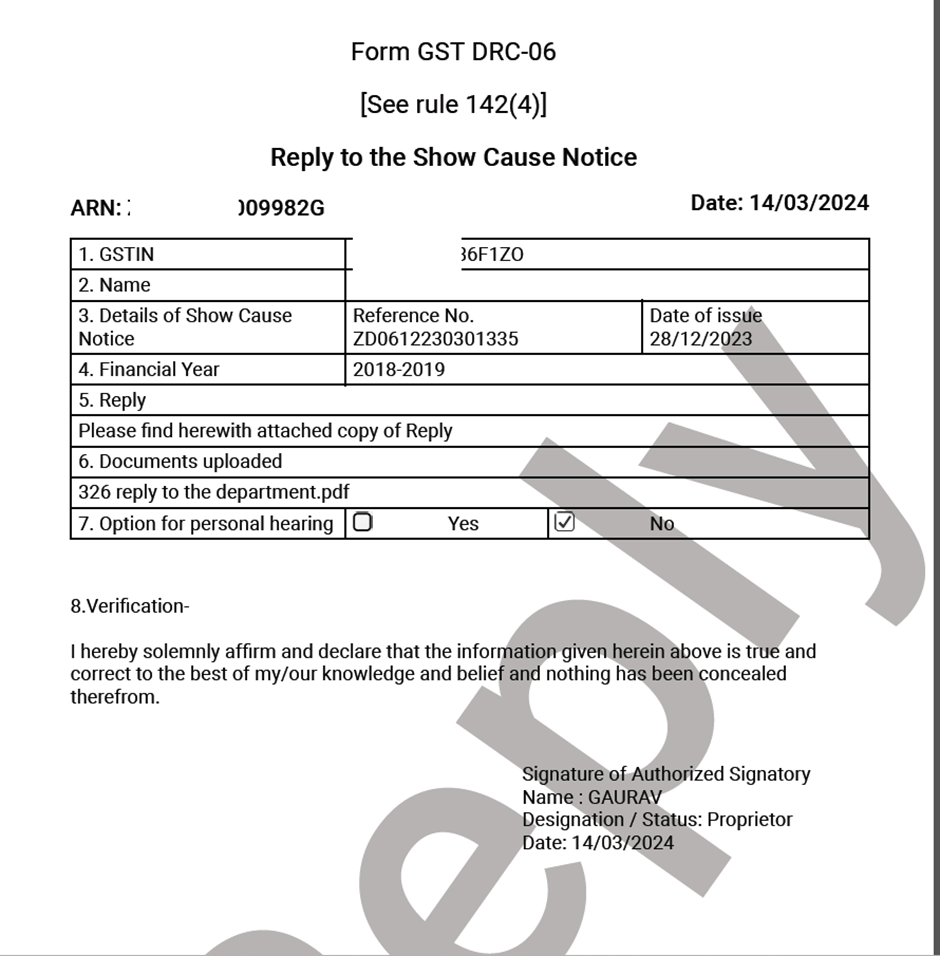

7. FORM GST DRC-06: Reply to Show Cause Notice

If the taxpayer receives FORM GST DRC-01 and wishes to contest the tax liability, they can respond using FORM GST DRC-06. This allows the taxpayer to submit a detailed explanation or provide documents justifying their position.

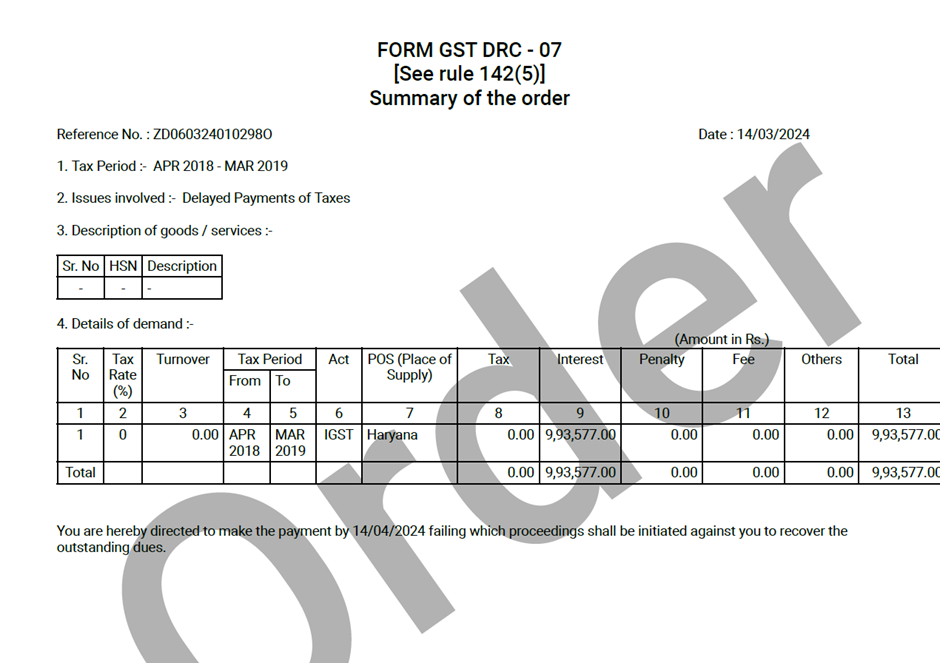

8. FORM GST DRC-07: Summary of Final Order

After evaluating the taxpayer’s response, the tax authorities issue FORM GST DRC-07, which summarizes the final order. This confirms the final liability, including tax, interest, and penalties, and can result in recovery action if the dues remain unpaid.

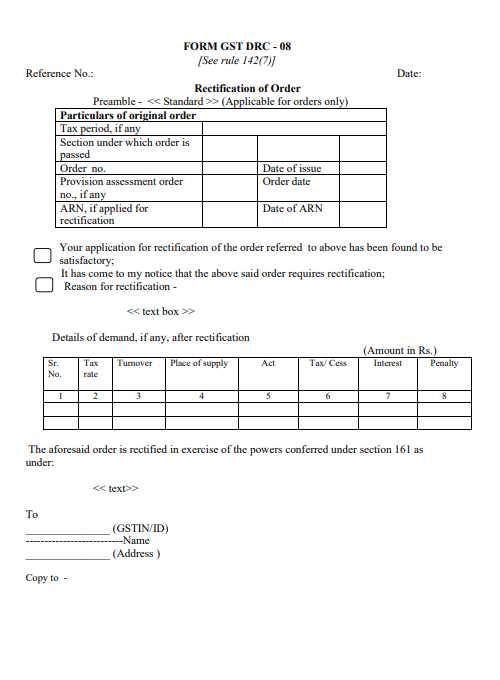

9. FORM GST DRC-08: Rectification of Errors

If any errors are found in the final order issued under FORM GST DRC-07, the taxpayer can request a rectification using FORM GST DRC-08.