Tax laws are not static; they evolve, adapt, and occasionally undergo amendments to accommodate changing economic landscapes and administrative requirements. Such is the case with the issuance of notices and orders under Sections 73 and 74 of the Central Goods and Services Tax Act, 2017 (CGST Act), which prescribe timelines for tax recovery and compliance procedures.

Table of Contents

Understanding the Timelines:

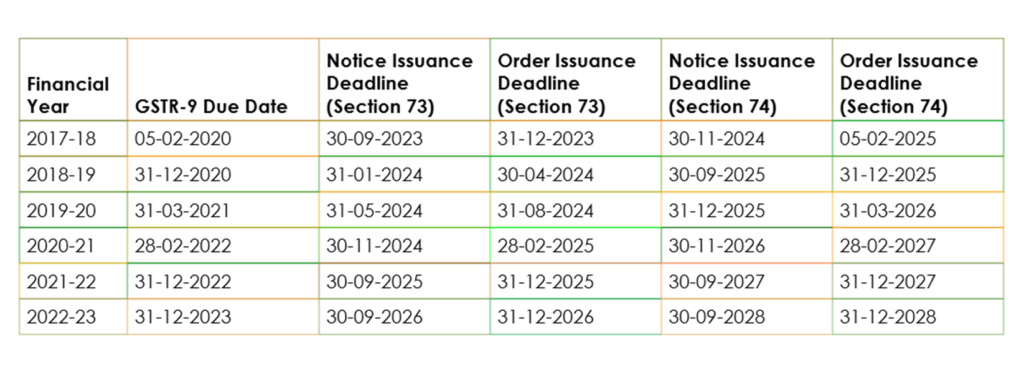

In a recent notification (No. 56/2023) dated 28/12/2023, the Central Board of Indirect Taxes and Customs (CBIC) extended the time limit specified under Section 73 for issuing orders related to tax recovery for certain financial years. Here’s a breakdown of the key deadlines:

Points to Remember

- Notification Reference: The notification referenced, No. 56/2023, is applicable solely to the financial years 2017-18, 2018-19, and 2019-20, specifically for Section 73.

- Tax Collected but Not Paid: If the demand pertains to tax collected but not paid under Section 76, there is no specific time limit set.

- Erroneous Refund: In cases of erroneous refund, the time limit is three years and five years from the date of refund, as applicable.

Full Article on Section 73 & 74